Historic economic expansion meets resistance.

2022 is another unpredictable year filled with great opportunity and change for our business community. Companies are seeing high demand for products and services, and the job market remains at historical levels for manufacturing, engineering, and architecture professionals. Meanwhile, waning pandemic disruptions and job and economic growth are meeting the headwinds of war in Europe, increased inflation rates, and exasperated supply chains.

Last November, we published The Konik Market Outlook for 2022, highlighting unprecedented talent demand, inflation warnings, the Great Resignations lingering effects, and the hottest skills for the year.

Here is our updated, mid-year outlook for the rapidly changing environment we’re navigating this quarter, focusing on three areas we believe will have a tremendous impact on the Midwest economy: Strong job market, inflation and interest rates, and supply chain forecasting.

Job market remains resilient:

The Midwest technical job market is expected to remain very strong over the next several months as architecture, manufacturing, and engineering companies keep hiring to meet relentless customer demand. While keeping an eye on broad economic indicators, our customers do not see a decrease in product and service demand. While some are becoming cautious with their hiring strategy, they continue hiring at all levels, including project architecture, construction project management, mechanical engineering, manufacturing, and automation.

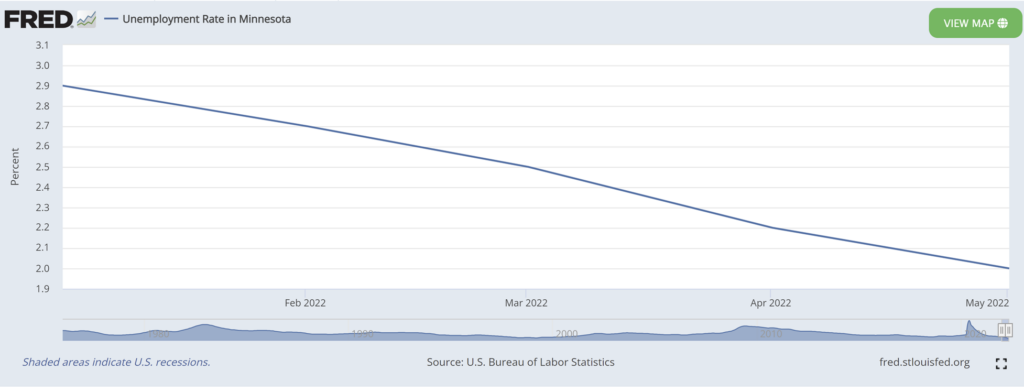

2022 Minnesota Unemployment Rate Trend to 2% (Federal Reserve of St. Louis)

Is the job market starting to cool?

We’re seeing limited hiring pauses and layoffs in a few areas, yet these are happening with larger companies outside the Midwest. While tech companies on the west and east coasts are making headlines for layoffs, we see a different story emerge here. We expect an overall strong demand for architecture, engineering, and manufacturing talent for the foreseeable future, while companies catch up on overdue projects and production backlogs. Particularly, multi-use rental housing construction fueled by rising mortgage rates, medical device manufacturing, and infrastructure sectors remain exceptionally busy this quarter.

The upside to a slowing job market will be slower inflation rates and lower prices on everyday goods and services. Our 2% unemployment rate, the lowest ever recorded, translates into increased salaries and benefits costs to companies. While this is very good news to an individual, it has unintended consequences for the overall economy as the costs are passed along to the consumer, and will require downward cycling to bring inflation under control.

Inflation and interest rates rise to the top of business issues

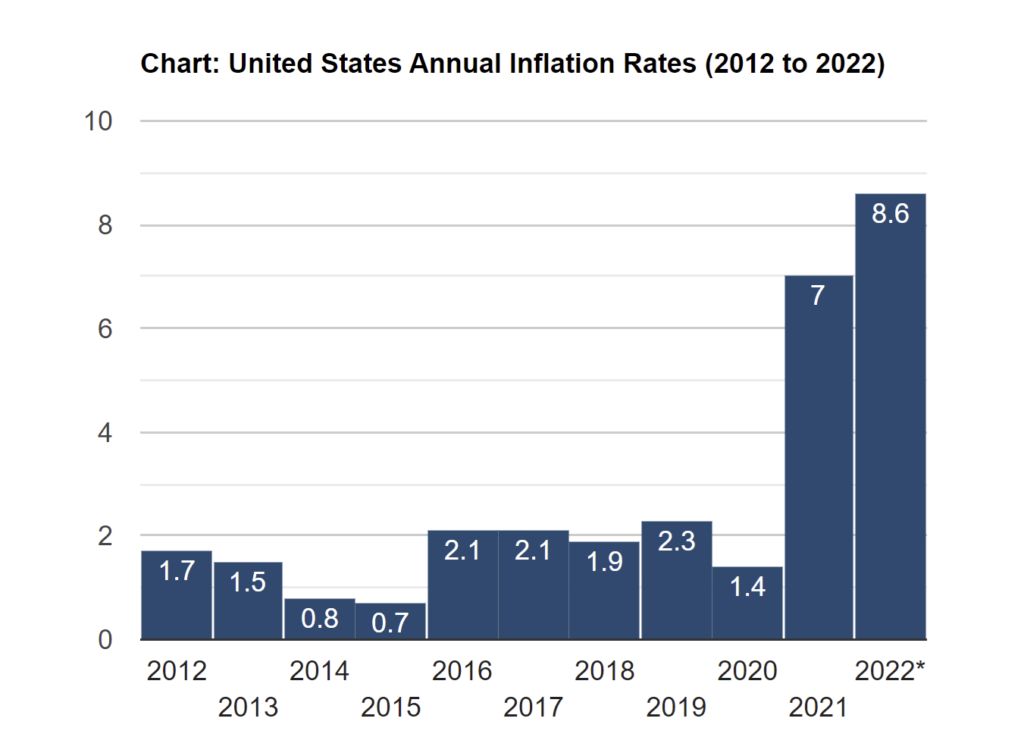

This time last year, hiring technical talent was easily the main reason executives and managers lost sleep. While finding talent is still top of mind, this has been replaced by rising business costs on everything from fuel, raw materials, and employee compensation. With inflation increasing to 8%, companies must take a critical look at their budgets and consider where to raise prices, save and spend cash and capital. Rising interest rates on property development, large equipment purchases, and investment capital is starting to set in and give executives reason to hold off or slow down business expansion plans.

The Federal Reserve’s actions to aggressively increase bank rates are a direct effort to slow economic growth and inflation. These Fed efforts will take several months to have a lasting effect and cool prices. Meanwhile, companies will spend more time discussing and executing ways to mitigate the effects of rising costs.

While this will dampen more bullish plans, we continue to expect companies to thrive in the quarters ahead and continue to meet customer demands and grow during this Federal Reserve cycle.

Supply chain forecasting is extremely critical

Perhaps most interesting and challenging about the changing market dynamics is its impact on supply chain, inventory, and supply forecasting. Companies have been waiting months and, in some cases, years for critical supplies to keep production moving and ship products to customers, all while demand in some industries is slowing. This, from our perspective, will be a very critical area to navigate and an area of focus over the next few months. Delayed shipping times can quickly become overstock headaches tying up massive capital and profits if companies are not careful and keep a close eye on this area.

We’re seeing some of this play out in Target Corporations’ recent shareholder announcements stating excessive inventory of Covid-driven items such as clothes, small home appliances, and furniture. Target is slashing prices of these items and ramping down new purchases as consumers switch their spending to travel, family experiences, and savings. Target’s situation may well be a warning to all inventory-dependent companies to tread carefully and read and react when necessary.

Many of Target’s manufacturing suppliers are left with canceled orders and a sharp decline in new business in a short period, creating havoc to balance sheets and revenue, requiring them to freeze hiring and decrease their raw material orders.

Companies must be vigilant of the Bullwhip Effect, where the demand variance travels upstream in the supply chain. Upstream consists of the retailer through to the wholesaler and manufacturer. The distortion is created by the variance of orders which may be larger than sales. The resulting effect can quickly bring overstock and liabilities before the company has time to react and change course.

For a more detailed look at forecasting, see our recent live event, “What’s to Come in Supply Chain 2022-2023”

Is a recession in our near future?

This question is asked more often lately and for a good reason. The changing economic conditions, recent Fed actions, a volatile stock market, and layoff headlines are reasons to be concerned. A recession is generally defined as a fall in GDP for at least two consecutive quarters. Many economists believe it’s extremely difficult to tame inflation without drastically slowing the economy. Q1 2020 realized a GDP decrease of 1.6, with Q2 forecasts showing a very small increase and potentially a decrease in GDP, resulting in a technical recession. We will see slowed economic activity over the next two quarters as the natural and engineered effects play out. Optimistically, we may fall short of a recession; however, a slowed economy and, at best, a soft landing is required before inflation comes down. Once inflation and extreme consumer spending calm down, we expect normalized activity in all areas, including job growth, lower gas prices, and inflation returning to 2-3%.

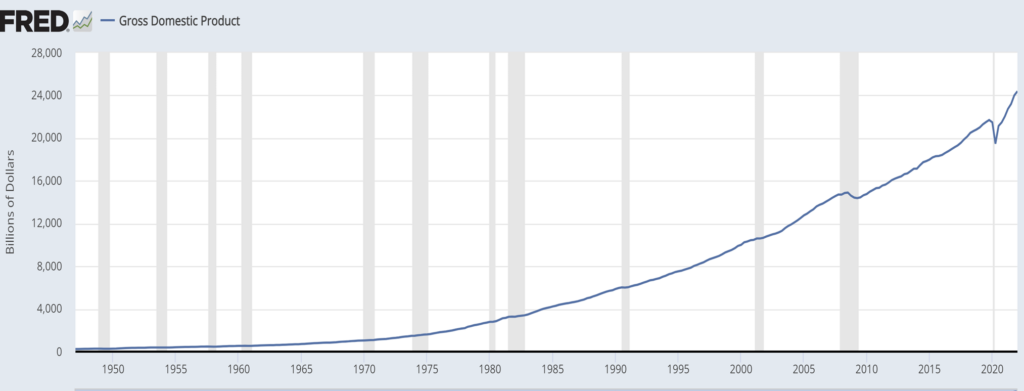

The power of the U.S. economic engine has been increasing for decades and is expected to continue after a brief pause or slight rest and recovery period. The graph below shows the US GDP increases since 1948, where the output of the U.S. grew to $23 Trillion in 2021. Looking beyond the next couple of quarters, our ability to return to growth is very evident. Our market economy has shown resiliency and rebounds after each setback and onward to another longer growth trajectory. Once post-pandemic demand decreases and inflation is managed, we will see a healthy return to the local market.

US GDP since 1948, $23 Trillion in 2021 (Federal Reserve of St. Louis)

Visit Konik Insights to learn more about the job market, leadership best practices, and career advice.

Konik is a technical recruiting and staffing company focused on manufacturing, engineering, and architecture careers in the Midwest.