The Konik Market Outlook for 2023

The greatest job market in history enters a new phase of slower growth.

As we begin the year, Konik looks ahead with our predictions for 2023 and reviews the ups and downs of this past year.

In our 2022 Market Outlook released in November 2021, we highlighted our thoughts on “Inflation, the 2022 word of the year”, “The Great Resignation,” and “The hottest skills” for last year. These themes played out much to our projections and will impact the new year.

Manufacturing and architecture services companies grew while hiring professionals at all levels to meet relentless customer demands. Degreed Engineers, Architects, and Construction professionals saw steady raises and larger-than-normal offers when switching companies. We’ve seen historic offer salaries for technical professionals from entry-level to management job functions, with salary jumps of 20% not uncommon in offer letters.

The U.S. is the largest economy in the world and proved once again to be incredibly resilient with a very strong growth ability. Despite significant supply chain disruptions, China’s Covid lockdowns, and an ongoing war in Europe, we’ve expanded in the face of these barriers and grew 23% since June 2020.

Here, we look ahead to what we can expect for 2023.

Our 2023 Job Market Outlook

We expect job growth to continue through much of 2023 – at a slower pace.

The Greatest Job Market in History Transitions.

Manufacturing (per thousands of persons):

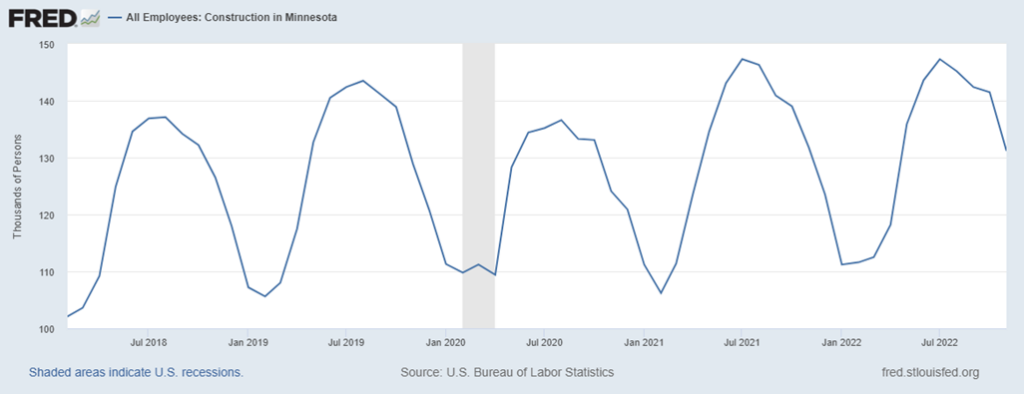

Construction (per thousands of persons):

We expect job growth to continue through much of 2023 – at a slower pace. The state and country have added jobs at a very healthy rate, yet recent months have seen a lower growth percentage month-over-month due to the Federal Reserve’s increased interest rate. The increased rates are lowering demand for products and services, which is the Fed’s intended effect. In turn, this results in a decreased need for employees. The Midwest manufacturing and construction sectors are not immune to the effects. Overall, local companies will grow, and many will even thrive in 2023, while others are slowing their hiring practices until more favorable environments return.

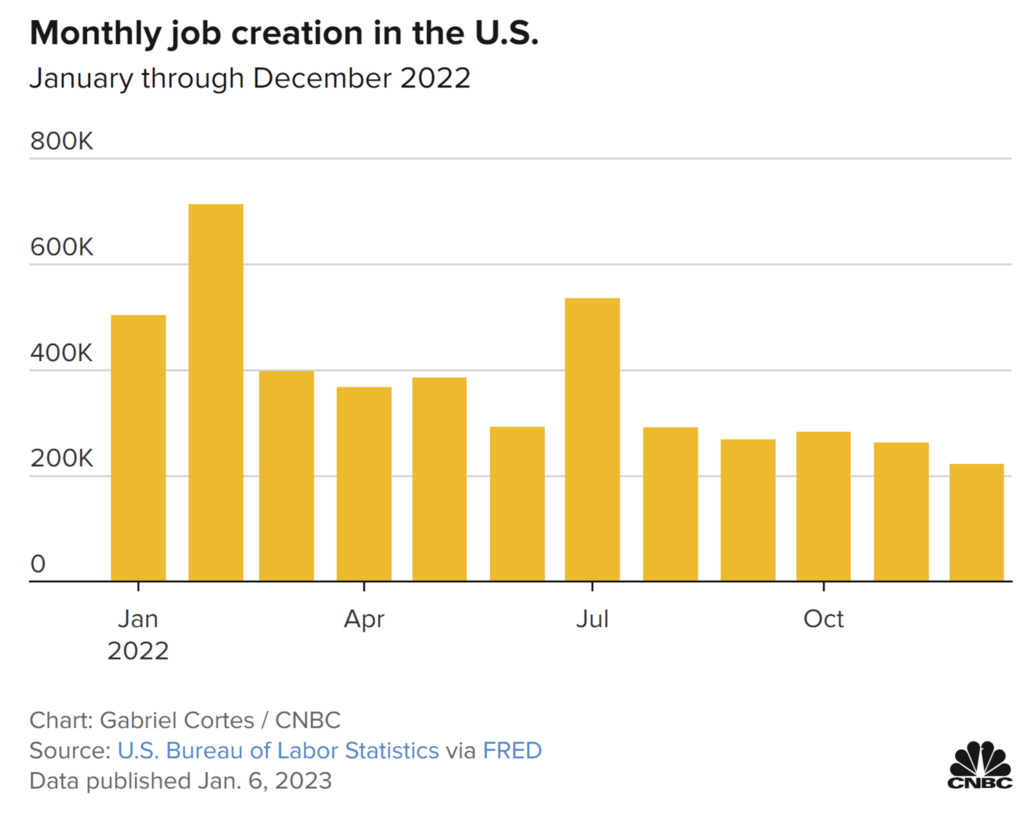

What seemed like an environment where every company was hiring a year ago is transitioning into a new phase. This year, fewer companies are hiring and doing so at a slower pace. Companies are being more cautious and reviewing budgets before adding new positions and backfilling replacements. As the CNBC graph shows below, we’re still adding jobs at a slower pace. This slower growth is expected to continue for much of the year.

Interest rates are expected to increase in the months ahead, then maintain at high levels for up to 12 months in an explicit Fed attempt to slow wage growth and bring inflation back down from 7% to 3%. The effect will mean new job growth will slow and even out the supply and demand economics of the current job market.

Will there be a recession in 2023?

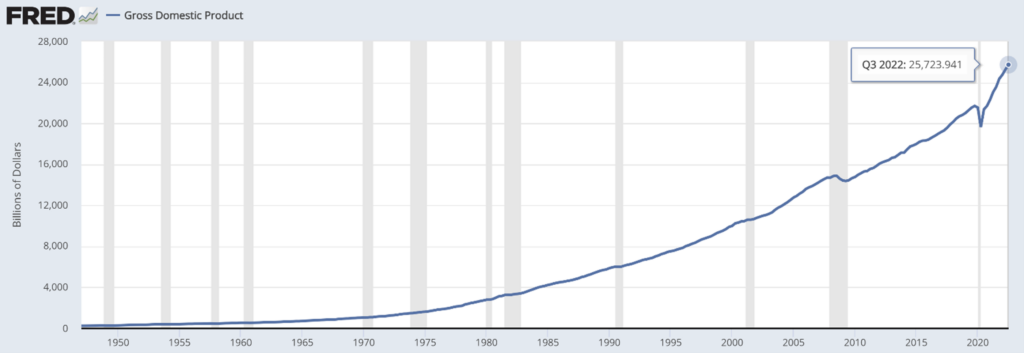

The US economy has grown 23% since June 2020. The overall economy is very healthy, even with a pullback this year.

No one knows for sure, but a recession seems more likely than not. A recession is generally defined as a fall in GDP for at least two consecutive quarters. On average, the U.S. has experienced a recession every seven years. We are taking out the two-month 2020 recession, which many consider a natural disaster event and not an economic one; the last recession ended in June 2009, or 13 years of economic expansion. With 2020 as an exception, we’re well overdue by six years per historical trends.

Economists agree it’s tough to tame inflation without drastically slowing the economy. The economy has been growing incredibly fast since the stimulus packages of 2020 and 2021, causing painful inflation. It’s becoming increasingly likely that we won’t bring inflation down to a healthy rate without one, or at best, several quarters of minimal growth. From there, the Fed can reduce rates, the supply chain disruptions will calm, and companies will hire talent more quickly and grow. In the meantime, we expect slower growth than last year, with the latter half being slower than the first and a higher risk of recession.

Zooming out, there are solid reasons for economic optimism. The US has seen a 23% growth in GDP since June 2020. Even with a pullback from this, the overall economy is very healthy. The Federal Reserve Bank of St. Louis chart shows that our overall GDP numbers have been solid. Even when a recession occurs, we’re expected to continue our upward trajectory.

What does this mean for the job market?

Naturally, as the overall economy goes, so does the overall job market. Our sector can expect to see a slower growth phase than we saw last year. Given 1.7 jobs per unemployed currently, we’ll see this ratio decline to a more even number. This means it’ll take longer for someone to find a new position once starting a search. Also, salary increases for new positions will be lower than we’ve recently seen. This will feel more like the job market of 2013-2017, where jobs were available, yet candidates didn’t have endless options.

Inflation Plateaus Then Declines

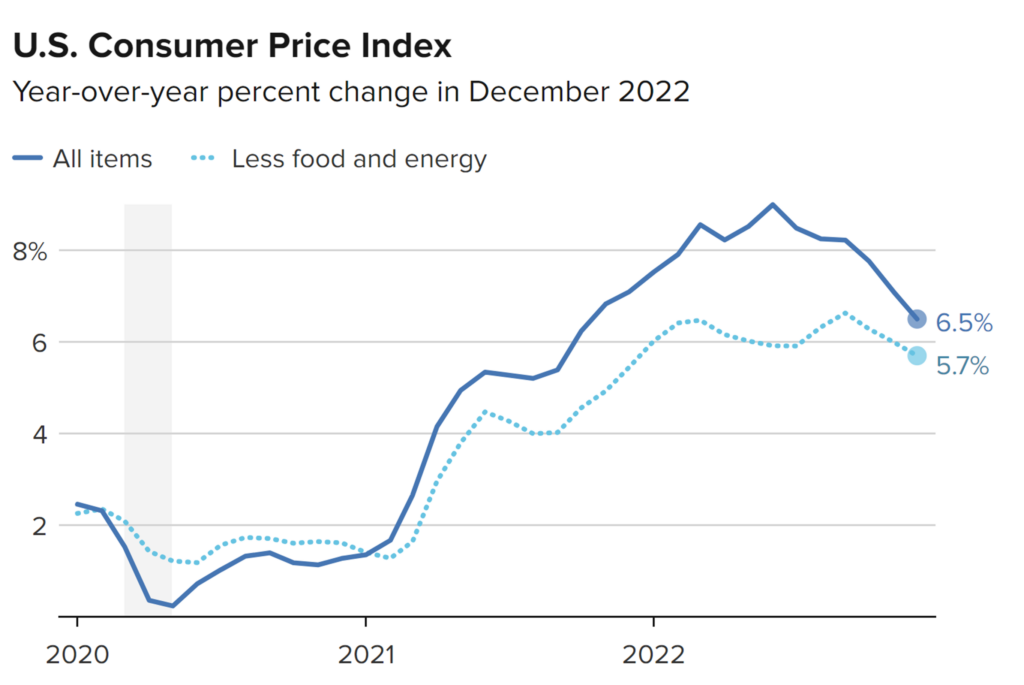

The latest federal jobs and inflation reports paint a more optimistic outlook on how the year will unfold. These reports indicate that worker wage increases are slowing and inflation is moderating. After peaking in mid-2022, as the chart from CNBC shows, inflation is decreasing and headed in the right direction. This is overall good news for everyone. Assuming this trend continues in the months ahead, the Fed will likely refrain from rate hikes and hold steady until a more normal 3% inflation rate returns.

The caveats of risk are always present. Additional geopolitical tensions around Taiwan, an expanded Ukraine conflict, and another Black Swan event like Covid can quickly chain this outlook. Barring this, we’ll see a moderation of both job market opportunities, lower wage increases, and inflation at a healthy rate of 2-3%.

What does this mean for the job market?

We expect a slow return to a normalized job market similar to 2013 – 2019, a slow, steady, and predictable environment. This means companies will hire cautiously and, overall, fewer opportunities for each job seeker. Professionals in the job market can expect great options, but they will be fewer, and the pace of hiring will be slower than in the last couple of years.

Pay increases will also peak and decline as the cost of living decreases in the months ahead. New job offer salaries will also moderate as hyper-demand for employees drops. Employees thinking about asking for a raise or finding a new role would benefit from doing this sooner rather than later.

The supply chain stabilizes with lingering headaches.

Disruptive supply chain issues, long delivery lead times, and unpredictable inventories pained manufacturing, engineering, and construction industries. Slowly, these also moderate with decreased demand and China removing lockdowns and work and travel restrictions. Manufacturing and construction supplies will flow more freely and quickly than they have since March 2020, and operations will become less disruptive and faster as a result.

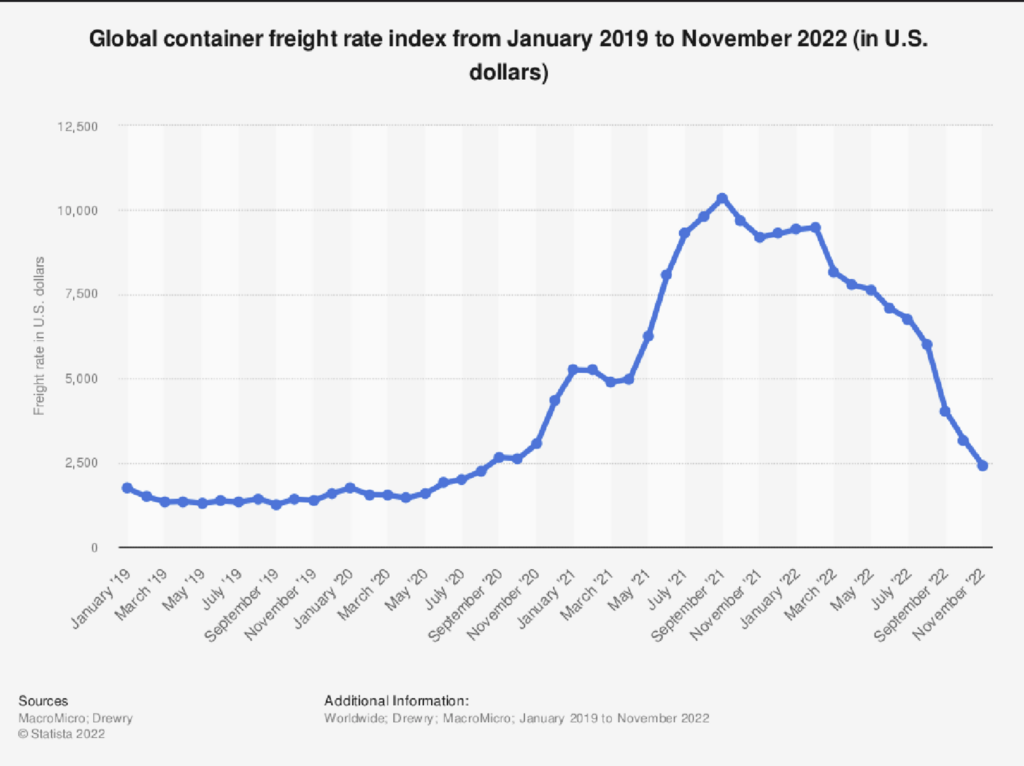

The chart below illustrates global demand for shipment crates returning to pre-pandemic levels resulting in faster deliveries and lowered prices for manufacturers and consumers

What does this mean for the job market?

Companies can move finished products to customers and manufacturing jobs more predictably, and production lines will run smoother. Demand for supply chain roles will continue; however, less focus will be on these areas. Longer-term planning, near-shoring, and supply analytics roles will continue to be in demand, yet not as urgent as in previous years.

Technical Job Market Remains Robust

Continued demand for engineering, manufacturing, and architecture employees remains.

Most industries will follow national trends, including manufacturing, engineering, and architecture. Some niches are more recession-proof than others, while others will be much more at risk of a deeper pullback. This largely depends on how each industry is affected by rising interest rates. Residential real estate industries and manufacturing and architecture firms that support them will be more affected than others. On the other hand, medical companies that develop non-elective products will be more resilient and experience steady growth in 2023. Another example is food manufacturers focusing on staple, and everyday items will be less impacted than others.

Continued demand for engineering, manufacturing, and architecture employees remains. Demand will be less, yet technical employees in this area are expected to prosper in the year ahead. Overarching factors such as lower technical college enrollment, an aging workforce, and slower legal immigration are expected to continue for the foreseeable future.

Related Insights:

“The Ultimate Job Description Guide”

“The Konik Market Outlook for 3rd Quarter of 2022”

Tom Goettl, President of Konik, a Technical Talent Network, writes at the intersection of careers, leadership and technology. Learn more about how we can help at www.konik.com